Mumbai. Updated on : Tuesday, 23 June 2026

The fiscal landscape in India is undergoing its most significant transformation in over six decades. Effective April 1, 2026, the New Income Tax Act 2026 (officially passed as the Income-tax Act, 2025) officially replaces the veteran 1961 Act.

Designed with a digital-first approach, this sweeping reform aims to clear out decades of legal clutter, offering the common taxpayer a transparent, readable, and highly rewarding tax structure. If you have been wrestling with complicated tax terms for years, this new framework is breath of fresh air. Let’s break down exactly what changes and how it impacts your wallet.

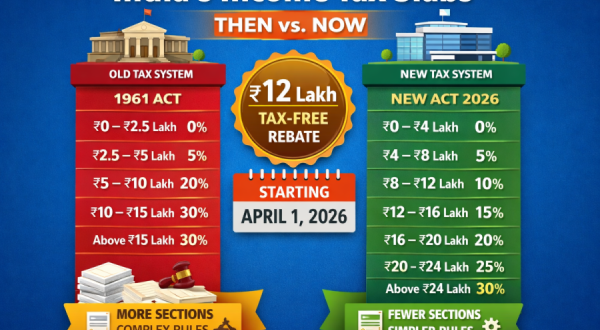

1. Major Relief: Zero Tax Up to ₹12 Lakh

The biggest celebration for the Indian middle class is the historic expansion of the Section 87A tax rebate. Under the New Tax Regime, which is now the default option for all taxpayers, resident individuals with a total income up to ₹12,00,000 will effectively pay zero tax.

Extra Perks for Salaried Individuals

If you are a salaried employee, the benefit stretches even further. By combining the zero-tax threshold with the newly adjusted Standard Deduction of ₹75,000, a gross salary of up to ₹12.75 Lakh becomes entirely tax-free!

How Marginal Relief Saves You from the “Tax Cliff”

In older tax structures, earning even a single rupee over a tax threshold could sometimes trigger a massive tax liability, a frustrating phenomenon known as a “tax cliff.”

To protect your hard-earned money, the government has introduced a robust marginal relief mechanism. This ensures that if your income marginally crosses the ₹12 Lakh mark, your total tax liability will never exceed the extra income you earned.

For instance, if you earn ₹12,15,000, your raw tax across the slabs would normally be ₹62,250. However, thanks to marginal relief, your tax before cess is strictly capped at the extra ₹15,000 you earned over the limit.

2. The New Tax Regime Slabs (Effective April 1, 2026)

The progressive tax slabs under the new act have been widened to ensure lower tax rates for lower income brackets. Here is how the income ranges are taxed:

| Income Range | Tax Rate |

| Up to ₹4,00,000 | Nil |

| ₹4,00,001 – ₹8,00,000 | 5% |

| ₹8,00,001 – ₹12,00,000 | 10% |

| ₹12,00,001 – ₹16,00,000 | 15% |

| ₹16,00,001 – ₹20,00,000 | 20% |

| ₹20,00,001 – ₹24,00,000 | 25% |

| Above ₹24,00,000 | 30% |

3. Structural Simplification & Digital Clarity

The 2026 Act isn’t just about tweaking numbers; it completely rewrites the rulebook to make tax laws comprehensible for everyday citizens, not just corporate lawyers.

-

Welcome the “Tax Year”: Say goodbye to the confusing, overlapping terms “Previous Year” (PY) and “Assessment Year” (AY). The new framework consolidates everything into a single, intuitive Tax Year.

-

Massive Section Consolidation: The total number of legal sections has been slashed from an overwhelming 800+ down to just 536. A prime example of this optimization is Section 393, which consolidates all Tax Deducted at Source (TDS) rules into a single, easily scannable table.

-

Modern Digital Rules: Reflecting India’s rapidly expanding digital economy, search and seizure laws now explicitly cover “information stored in electronic media,” ensuring seamless compliance and transparent tracking.

4. Boosted Allowances for Salaried Employees

To account for inflation and changing urban demographics, several long-standing allowance limits have received a massive, overdue boost:

-

HRA Metro Expansion: Bengaluru, Hyderabad, Pune, and Ahmedabad have officially been added to the Metro Cities list. Salaried individuals renting homes in these tech hubs can now claim a 50% basic salary exemption for House Rent Allowance (HRA), up from the previous 40%.

-

Children’s Education Allowance: Increased significantly from a legacy rate of ₹100 per month to ₹3,000 per month.

-

Hostel Allowance: Bumped up from ₹300 per month to ₹9,000 per month.

-

Tax-Free Meal Vouchers: The daily limit for employer-provided meals has been raised to ₹200 per meal.

5. Timeline: Navigating the Transition

While the law officially changes on April 1, 2026, the structural shift for your filings will be gradual:

-

July 2026 Filing: When you file your returns in mid-2026, you will still be reporting income earned during the financial year 2025-26 under the old Income Tax Act of 1961.

-

July 2027 Filing: This will mark your historic first time filing tax returns using the streamlined, simplified forms of the New Income Tax Act 2026.

-

Legacy Disputes: Any active tax disputes, audits, or assessments relating to financial years prior to April 2026 will continue to be processed under the regulations of the old 1961 law.

Alt Image Text Descriptions for Visual Elements

-

Infographic Image: A clear, colorful tax slab infographic detailing the New Income Tax Act 2026 tax rates ranging from 0% for income under ₹4 Lakh up to 30% for income above ₹24 Lakh.

-

Conceptual Image: A happy Indian salaried professional working on a laptop, calculating middle-class tax savings under the expanded Section 87A rebate.

Frequently Asked Questions (FAQ)

Q1: Is the Old Tax Regime still an option under the 2026 Act?

The New Income Tax Act 2026 establishes the simplified structure as the absolute default regime. The legacy 1961 Act is being fully repealed, making the new structural slabs the unified path forward for tax filing.

Q2: How exactly does Marginal Relief work if I earn ₹12.10 Lakh?

Without relief, an income of ₹12.10 Lakh would push you out of the zero-tax bracket, creating a standard tax of ₹61,500. With marginal relief, your tax is strictly capped at the extra amount you earned above the threshold (₹10,00,0). Thus, your net tax drops from ₹61,500 to just ₹10,000 (plus 4% cess).

Q3: When can I start claiming the higher HRA for Bengaluru or Hyderabad?

The 50% basic salary exemption for the newly added metro cities takes effect for the income you earn starting April 1, 2026. You will enjoy this benefit throughout the tax year and see it reflected when you file under the new act in July 2027.

Relevant Regional Information

For the latest local updates, regional administrative circulars, and analytical breakdown of fiscal updates translated across India, visit the official English portal at Matribhumi Samachar.

Disclaimer: This article is compiled for informational and educational purposes only. It does not constitute legal, financial, or investment advice. Tax laws are subject to dynamic updates; please consult a certified Chartered Accountant or a registered financial advisor before making tax planning or investment decisions.