Mumbai. Updated on : Tuesday, 23 June 2026

Securing a piece of real estate in India’s booming urban hubs has changed dramatically. If you are looking to buy a home, your financial health is no longer evaluated on a curve. It is judged by a rigid, automated system where a few points on your credit score can cost or save you lakhs of rupees.

With the Reserve Bank of India (RBI) adjusting the repo rate to 5.25%, home loan affordability has technically improved. However, banks are keeping the velvet rope up: these sweet interest rates are strictly reserved for the most credit-disciplined borrowers.

The 2026 Benchmark: Why 750 is the New 700

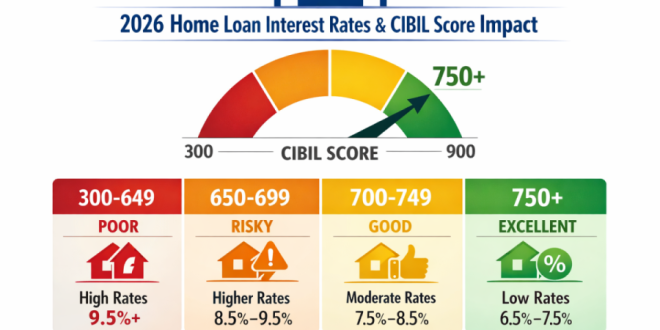

Historically, a CIBIL score of 700 was considered “good enough” to get you through the door at most major financial institutions. That is no longer the case.

Top-tier lenders like SBI, HDFC, and ICICI Bank have tightened their automated underwriting algorithms. The coveted “star” interest rates—currently hovering at an attractive 7.1% to 7.5%—are exclusively unlocked if your CIBIL score is 750 or above.

If your score dips below this threshold, you enter the territory of risk-based pricing. Borrowers with scores below 650 face steep interest premiums, with rates climbing as high as 9.5% to 11%. Over a standard 20-year tenure, the difference between an average score and an excellent score can easily translate to over ₹5 Lakh in extra interest payments.

3 Critical Factors Triggering 2026 AI Risk Models

Today’s lending ecosystem relies heavily on automated risk assessments. To maximize your home loan eligibility, you need to manage the core pillars of your credit report with precision:

1. The 30% Credit Utilization Guardrail (30% Weightage)

Maxing out your credit cards is an immediate red flag for modern risk engines, signaling “credit hunger.” To protect your score, keep your total credit usage below 30% of your available limit across all cards.

-

Pro-Tip: If your billing cycle ends on the 20th, pay off your balances by the 15th so a lower utilization rate is reported to TransUnion.

2. Defeating the “Settled” Status Trap

If you have old, unresolved debts, do not fall for a quick compromise. When a bank offers to “settle” a loan by waiving off a part of your interest or principal, your report gets marked as “Settled.”

-

This tag acts as a severe warning sign to future lenders and remains on your profile for 7 years.

-

Always opt for a “Closed” status by paying the debt in full and securing a formal No Dues Certificate (NDC).

3. Clearing Out “Ghost Accounts”

Administrative errors happen more often than you think. A “Ghost Account” is an old loan or credit card that you have completely paid off, but due to a banking glitch, it still appears as “Active” or “Written-Off” on your TransUnion report. Routinely audit your credit profile and raise immediate disputes on the CIBIL portal to wipe these errors clean.

Actionable Tips to Boost Your Eligibility Right Now

-

Apply with a Co-Applicant: If your individual score is lingering in a gray area, adding a co-applicant (like a spouse or parent) with a stable income and an excellent credit history can bypass strict individual score hurdles.

-

Observe the 6-Month Cooling Period: Refrain from applying for new credit cards, personal loans, or “Buy Now, Pay Later” (BNPL) schemes for at least six months before your home loan application. Every application triggers a “hard inquiry,” shaving valuable points off your score.

-

Leverage New Transparency Rules: Under the latest 2026 home loan guidelines, lenders are legally mandated to return your original property documents within 30 days of loan closure. If they delay, they must pay a daily penalty to you. Keeping a clean, trackable “Closed” status on your ongoing debts makes you a highly favorable candidate for these strictly regulated banks.

Frequently Asked Questions (FAQs)

1. Can I get a home loan in 2026 with a CIBIL score of 680?

Yes, but you will likely miss out on the lowest “star” rates (7.1%–7.5%). Lenders will classify you under risk-based pricing, meaning you will face higher interest rates or be redirected to Non-Banking Financial Companies (NBFCs) with more stringent terms.

2. How much can I save by improving my score from 700 to 760?

On a standard 20-year tenure, moving from an average interest rate bracket to a prime “star” rate can save you upward of ₹5 Lakh in interest outgo, depending on your total loan amount.

3. What should I do if a bank refuses to update my “Settled” status to “Closed”?

If you have paid the entire outstanding amount, submit your No Dues Certificate (NDC) and payment receipts directly to the CIBIL dispute resolution portal online. By law, errors must be investigated and resolved within 30 days.

Relevant Resources

To keep track of your financial profile and stay ahead of the market, check out these deep dives from Matribhumi Samachar:

-

Free Credit Tracking: Learn how to monitor your rating securely via Matribhumi Samachar: How to Check Your CIBIL Score Online for Free.

Disclaimer: This report is for informational purposes only and does not constitute financial or investment advice. Interest rates, repo rates, and banking policies are current as of April 2026 and are subject to market changes and RBI regulations. Please verify all slab-based interest calculations and safety guidelines directly with certified financial consultants or your respective lenders before signing a loan agreement.