Mumbai. Updated on : Tuesday, 23 June 2026

As we navigate the second quarter of 2026, the Indian banking sector is experiencing a massive paradigm shift. With the Reserve Bank of India (RBI) maintaining the benchmark repo rate at 5.25% following the February 2026 Monetary Policy Committee (MPC) meeting, a unique wealth-building window has opened wide for everyday retail depositors.

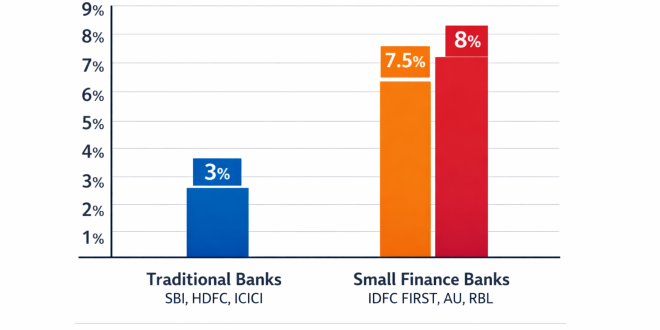

While traditional banking titans like State Bank of India (SBI) and HDFC Bank offer unmatched institutional stability, their modest returns of 2.5% to 3.5% fail to outpace inflation, which is projected at 4.0% for Q1 2026-27. Leaving significant cash reserves in these accounts means your money is actively losing purchasing power.

Fortunately, a new league of “yield disruptors”—primarily composed of Small Finance Banks (SFBs) and agile mid-sized private lenders—is helping savvy Indians earn up to 8.00% per annum on liquid cash.

The 2026 Yield Leaderboard: Top Banks Offering High Interest Rates

The battle for retail deposits has intensified. To secure liquid funds, several institutions have significantly scaled up their yields. If you are looking for the best high-interest savings account in India for 2026, these are the primary contenders:

| Bank Name | Max Interest Rate (p.a.) | Standout Feature |

| DCB Bank | 8.00% | Industry-leading peak rates for balances above ₹10 Lakh. |

| Equitas Small Finance Bank | 7.80% | Premium yields tailored for specialized wealth segments. |

| RBL Bank | 7.50% | High returns optimized for balances between ₹25 Lakh and ₹2 Crore. |

| AU Small Finance Bank | 7.25% | Consistent monthly interest payouts for balances exceeding ₹10 Lakh. |

| IDFC FIRST Bank | 7.25% | Unique monthly compounding frequency that elevates the effective yield. |

| IndusInd Bank | 7.00% | Excellent digital-first banking interface paired with tiered high returns. |

Unmasking the “Up To” Trap: How Progressive Interest Slabs Work

A common misconception among retail depositors is that the advertised “peak” interest rate applies flatly to the entire account balance. In 2026, almost all mid-sized private lenders and SFBs utilize a strict progressive slab system.

Under a progressive mechanism, your balance is split across different interest brackets.

A Typical Example: If a bank advertises 7.50% for balances between ₹25 Lakh and ₹2 Crore, your capital is not uniformly calculated at 7.50%.

-

Your first ₹1 Lakh might only earn a baseline 3.50%.

-

The incremental amount from ₹1,00,001 up to ₹25 Lakh might earn 6.00%.

-

Only the remaining balance above the ₹25 Lakh threshold qualifies for the prized 7.50% rate.

When you factor in these buckets, your real effective yield on a total deposit of ₹30 Lakh will actually hover near 6.05%. Always request an effective yield breakdown from your branch before moving your funds.

The Strategic Advantage of Monthly Payouts vs. Quarterly Compounding

Beyond the nominal percentage rate, the frequency of your interest credits dictates how fast your money grows. Traditional banking structures favor quarterly interest payouts, but disruptors like IDFC FIRST and AU Small Finance Bank have gained massive traction by implementing monthly interest compounding.

Mathematically, increasing the compounding frequency ($n$) within the compound interest formula yields a higher final balance ($A$), even if the base interest rate ($r$) remains exactly the same:

A = P(1 + r/n)nt

The Math in Action: Monthly vs. Quarterly Payouts

Let’s look at a practical scenario. If you maintain a balance of ₹5,00,000 at a 7.00% annual interest rate for 1 year:

-

Standard Quarterly Compounding ($n = 4$): You finish the year with ₹5,35,929.50 (Total interest: ₹35,929.50).

-

Disruptor Monthly Compounding ($n = 12$): You finish the year with ₹5,36,145.00 (Total interest: ₹36,145.00).

By simply picking a bank that calculates and deposits interest monthly, you bag an extra ₹215.50 on the exact same five-lakh deposit without sacrificing a single day of capital liquidity.

Safety First: Mastering the DICGC Risk Blanket in 2026

When hunting for high yields, safety should never take a back seat. A critical regulatory pivot to keep in mind is the recent implementation of the Risk-Based Premium (RBP) framework by the Deposit Insurance and Credit Guarantee Corporation (DICGC), which officially went live on April 1, 2026. This mandate ensures that banks with robust risk management frameworks pay lower premiums, fundamentally strengthening the safety profile of smaller lenders.

-

The Core Coverage: Every single depositor remains legally insured for up to ₹5 Lakh (encompassing both principal and accrued interest) per individual bank.

-

The Strategic Distribution Play: To completely protect a larger corpus of idle cash, financial planners advise against placing all your capital into a single institution. Instead, scatter your funds across 2 to 3 high-yield banks. Keeping individual balances below ₹4.5 Lakh across separate entities ensures your entire portfolio remains 100% insured under the legal DICGC umbrella.

Frequently Asked Questions (FAQs)

1. Are Small Finance Banks as safe as major commercial banks like SBI or ICICI?

Yes, Small Finance Banks (SFBs) are fully regulated by the RBI and hold scheduled bank status. Crucially, they are covered under the exact same DICGC insurance scheme as traditional banking giants, legalizing a safety net of up to ₹5 Lakh per depositor, per bank.

2. Can the bank change my savings account interest rate without warning?

Savings account interest rates are floating and subject to deregulation. Banks can alter their tier slabs or underlying percentage rates based on their internal liquidity needs or broader changes to the RBI repo rate.

3. How is the interest earned on a savings account taxed in India?

Under Section 80TTA of the Income Tax Act, interest earned on savings accounts up to ₹10,000 per year is completely tax-exempt for individuals under 60 years of age. For senior citizens, Section 80TTB extends this exemption up to ₹50,000 across all deposits. Any interest income exceeding these limits is taxed at your applicable slab rate.

Important Disclaimer

This report is compiled exclusively for informational and educational purposes and does not constitute a formal recommendation or financial advice to invest. Interest rates, slab structures, and regulatory rules are fluid and current as of Q2 2026. They remain subject to abrupt modifications by individual banking institutions or the RBI. Past performance or historic yields do not guarantee future returns. Always cross-verify actual slab calculations and current DICGC safety parameters directly with your respective banking partner or a certified financial consultant before opening an account.

External References & Resources

For further updates on national banking regulations, regional deposit trends, and real-time financial shifts in India, explore the following verified coverages from our regional desks: