Mumbai. Thursday, 23 April 2026

As we move through 2026, the Indian banking landscape has shifted from merely offering “no-minimum balance” accounts to providing comprehensive “Digital-First” financial ecosystems. Gone are the days when a zero balance account meant a “no-frills” experience with limited access. Today, banks are competing to offer premium features—like AI-driven expense tracking, high-yield interest, and seamless cross-border UPI—to customers who maintain a ₹0 balance.

Key Market Insights & Corrections

While the popularity of these accounts is surging, there are critical nuances often overlooked in general guides:

-

The BSBDA vs. Digital Savings Distinction: Many users confuse the Basic Savings Bank Deposit Account (BSBDA) with Digital Savings Accounts. BSBDA is a regulatory requirement by the RBI for financial inclusion, capped at 4 withdrawals monthly. Digital accounts (like Kotak 811) are commercial products that often allow unlimited digital transactions but may charge for physical services.

-

Virtual vs. Physical Plastic: In 2026, “Zero Balance” often applies to the account itself, but the Physical Debit Card is rarely free. Most banks charge an annual maintenance fee ranging from ₹199 to ₹599. If you are a UPI-only user, opting for the “Virtual Card” only is the true way to keep costs at zero.

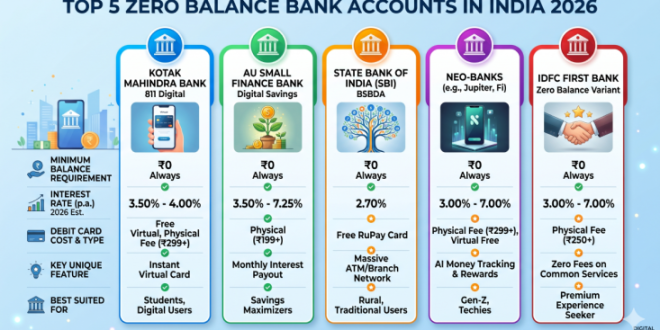

Top 5 Zero Balance Accounts Compared (2026 Edition)

1. Kotak Mahindra Bank: 811 Digital

The 811 account remains the market leader due to its frictionless Video KYC and “Dream Different” credit card options for zero-balance holders.

-

Best For: Students and Digital Nomads.

-

Latest Feature: Integrated “ActivMoney” which automatically moves surplus funds into a FD-like interest rate (up to 7%) while keeping the balance liquid.

2. AU Small Finance Bank: Digital Savings

AU Bank has disrupted the traditional players by offering high interest rates usually reserved for large deposits.

-

Best For: Maximizing returns on idle cash.

-

Latest Feature: Monthly interest payouts and a dedicated lifestyle app that offers hyper-local discounts on dining and travel.

3. State Bank of India (SBI): BSBDA

The most “democratic” account in India. It remains the only account where even the physical RuPay card and cheque books (for the first 10 leaves) are often provided with minimal or no charges.

-

Best For: Rural users and those seeking maximum security.

-

Latest Feature: Enhanced “YONO 2.0” integration allowing biometric-only ATM withdrawals (cardless).

4. Jupiter & Fi (Federal Bank Partners)

These neo-banking platforms have matured in 2026, offering the best UI/UX in the industry.

-

Best For: Gen-Z and Salaried professionals wanting automated savings.

-

Latest Feature: “Community Investing” where users can round up their UPI spends and automatically invest in Gold or Mutual Funds.

5. IDFC FIRST Bank: Zero Balance Variant

Known for its customer-centric approach, IDFC offers a premium feel even at zero balance.

-

Best For: Users who want “Private Banking” service without the high-balance requirement.

-

Latest Feature: Zero fees on most “Common Services” like IMPS, NEFT, and SMS alerts.

Important Considerations Before Opening

-

KYC Validity: Digital accounts opened with “Aadhaar OTP” are valid for only one year. To keep the account active permanently, you must complete Video KYC or visit a branch.

-

Transaction Fees: While the balance is zero, “Non-Financial” transactions (like getting a physical statement at a branch) or “Declined Transactions” due to insufficient funds often carry heavy penalties.

-

Nomination: Always ensure a nominee is added during the digital onboarding process to avoid legal hurdles for your family later.

Relevant News & Links

For more localized updates on Indian banking regulations, financial inclusion schemes, and local economic impact, explore the following resources:

-

Latest on Digital India Initiatives: matribhumisamachar.com/en/india-news

-

Financial Literacy & Consumer Rights: matribhumisamachar.com/en/business

-

Technology in Banking: matribhumisamachar.com/en/tech