Mumbai. Thursday, 25 June 2026

The digital revolution has transformed how we handle money in India. With Unified Payments Interface (UPI), mobile banking apps, and internet banking at our fingertips, managing finances has never been more convenient. However, this convenience also introduces risk. To safeguard millions of bank customers, the Reserve Bank of India (RBI) continuously updates its robust consumer protection framework.

Understanding these regulations is your best line of defense against financial fraud, unfair charges, and banking disputes. This detailed guide breaks down the critical RBI rules every account holder must know to ensure a secure financial journey.

1. The RBI Charter of Customer Rights

The bedrock of consumer protection in Indian banking is the RBI’s Charter of Customer Rights. Every bank operating in India is mandated to integrate these five core principles into their daily operations and customer interactions:

-

Right to Fair Treatment: Banks cannot discriminate against customers based on gender, age, religion, or physical ability. Both the bank and its agents must treat you with courtesy and respect.

-

Right to Transparency and Honest Dealings: All terms, conditions, interest rates, and processing fees must be disclosed upfront. Hidden charges or fine print that misleads the consumer are strictly prohibited.

-

Right to Suitability: Banks cannot aggressively push or “mis-sell” financial products (such as insurance or mutual funds) that do not fit your financial profile or needs.

-

Right to Privacy: Your personal and financial data must be kept strictly confidential unless you provide explicit consent or disclosure is legally mandated.

-

Right to Grievance Redressal: Banks are legally obligated to provide an easily accessible platform for lodging complaints and resolving them within a specified timeframe.

2. Navigating Online Fraud: Your Liability Limits

One of the most vital rules established by the RBI governs unauthorized digital transactions. If a fraudster steals money from your account via UPI, net banking, or credit card, your financial liability depends almost entirely on how quickly you act.

The 3-Day Window for Zero Liability

If you suffer a financial loss due to a security breach within the banking system, or if a third-party breach occurs and you report it to the bank within 3 working days, you have Zero Liability. The bank is required to reverse the entire lost amount back into your account.

Limited Liability Slabs (4 to 7 Days)

If the delay in reporting is on your part and you notify the bank between 4 to 7 working days after receiving the transaction alert, your liability is capped based on your account type:

| Account / Card Type | Maximum Customer Liability |

| Basic Savings Bank Deposit (BSBD) Accounts | ₹5,000 |

| Standard Savings Accounts, Credit Cards (limit up to ₹5 Lakh), Prepaid Wallets | ₹10,000 |

| Premium Credit Cards (limit above ₹5 Lakh), Current Accounts | ₹25,000 |

If you report the fraud beyond 7 working days, your reimbursement will depend entirely on your specific bank’s board-approved consumer protection policy.

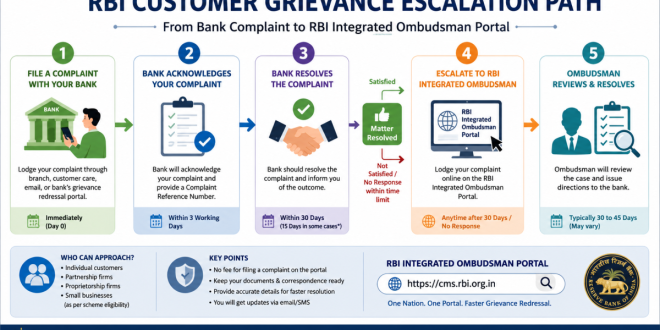

3. Step-by-Step Grievance Redressal: The Escalation Path

If you face issues like unauthorized electronic debits, wrong fee deductions, or poor service, you can enforce your rights through a structured escalation process.

Step 1: File an Internal Complaint

Your first step must always be to submit a formal written complaint directly to your bank’s customer service desk or branch manager. Ensure you collect a grievance tracking ID or an acknowledged copy of your letter.

Step 2: The 30-Day Resolution Window

The bank is legally given a 30-day “cooling period” to investigate your issue and offer a formal resolution or explanation.

Step 3: Escalate to the RBI Integrated Ombudsman

If the bank rejects your complaint, offers an unsatisfactory solution, or fails to reply at all within 30 days, you can escalate the matter for free. File a case online via the official RBI Complaint Management System (CMS) portal at cms.rbi.org.in. The Integrated Ombudsman acts as a neutral third-party arbitrator to resolve disputes fairly without any legal costs to the consumer.

4. Say No to “Mis-Selling” of Financial Products

A frequent complaint among Indian banking consumers is “bundling” or mis-selling. For example, a branch executive might insist that you purchase a specific life insurance policy to get a home loan approved, or force you to buy a mutual fund scheme to allocate a locker.

Under RBI guidelines, this practice is strictly illegal. Banking services cannot be made conditional upon purchasing third-party investment products. You have the full right to decline these products and report the branch if they refuse service.

5. Mandatory KYC: Identity Protection

Know Your Customer (KYC) guidelines are not just administrative hurdles; they are designed to prevent identity theft, money laundering, and financial fraud. Banks are required to verify your identity when opening an account and periodically update these records.

When updating your KYC, ensure you only submit Officially Valid Documents (OVDs) such as a Passport, Driving Licence, Voter ID card, or Proof of Address through verified, secure banking channels. Never send these documents via unverified WhatsApp links or third-party emails.

6. Best Practices for Safe Digital Banking

While the RBI provides a strong safety net, practicing preventative security habits remains your best defense against financial cybercrime:

-

Enable Instant Alerts: Always keep SMS and email transaction notifications active. If an unauthorized transaction occurs, these alerts ensure you can catch it instantly and leverage the 3-day zero liability rule.

-

The Golden Rule of Credentials: No legitimate bank official, customer care executive, or RBI representative will ever ask for your UPI PIN, ATM PIN, Online Banking Password, CVV, or OTP. Never share these digits with anyone.

-

Verify Links and Apps: Avoid clicking on hyperlinks sent via SMS or email claiming your account is blocked. Always navigate directly to your bank’s official website or use their verified mobile application from official app stores.

Frequently Asked Questions (FAQ)

What is the RBI Integrated Ombudsman Scheme?

The Integrated Ombudsman Scheme is a centralized mechanism set up by the RBI to resolve customer complaints against banks, Non-Banking Financial Companies (NBFCs), and digital payment system participants free of cost, provided the bank fails to resolve the issue within 30 days.

Will I get my money back if I accidentally share my OTP?

If a customer shares their OTP or passwords, it is classified as customer negligence. However, under standard guidelines, if you report the fraud immediately, banks are still mandated to assist in blocking the channels to minimize further loss. Additionally, prompt reporting within 5 days can still help genuine victims recover partial losses under localized cybercrime and bank mitigation policies.

Can a bank charge me for keeping a low balance without warning?

No. RBI rules dictate that banks must notify customers via SMS or email the moment their account balance falls below the required minimum. The bank must give the customer a grace period of one month to restore the balance before levying any penalty charges.

Disclaimer

The information provided in this article is for educational and general awareness purposes only. While every effort has been made to ensure accuracy based on current RBI circulars and regulatory guidelines, banking rules are subject to change. Readers are advised to cross-verify specific compliance details and terms with their respective banking institutions or the official Reserve Bank of India website.

-

Relevant Context: To discover local hyper-localized reports, financial regulatory updates, or regional perspectives on community banking in India, you can check the latest English publications directly on Matribhumi Samachar.