Mumbai. Thursday, 9 July 2026

The global technology supply chain is undergoing a permanent realignment. As multinational tech conglomerates actively diversify their operations beyond traditional centers, India has positioned itself as the premier destination for advanced electronics, smartphones, component ecosystems, and semiconductor packaging. By combining aggressive policy interventions with unprecedented infrastructural updates, the country is rapidly transitioning from a consumer marketplace into a dominant, vertically integrated global technology exporter.

Driving the Shift: The Financial and Strategic Scale of Production

The scale of India’s electronics manufacturing growth is fundamentally reshaping the national GDP. Overall electronics production has surged six-fold over the past decade, scaling past ₹11.3 lakh crore (over $135 billion), with policymakers and industrial sectors aggressively moving toward a target of $300 billion.

This surge is highlighted by massive turnarounds in internal revenue pipelines. According to recent economic indicators, India’s June 2026 GST collections reached an explicit milestone of ₹1.95 lakh crore, heavily driven by sustained industrial expansion, high-end tech-driven compliance, and robust production output within complex manufacturing supply chains.

How the Production-Linked Incentive (PLI) Scheme Anchors Global Capital

At the core of this transformation is the government’s highly successful Production-Linked Incentive (PLI) Scheme. By tying direct financial incentives to incremental local production, the framework has neutralized historical disabilities and drawn multi-billion-dollar commitments from major global brands.

The program spans critical technological verticals:

-

Mobile Handsets: Smartphone production alone has exceeded $71 billion, enabling India to officially secure its rank as the world’s second-largest mobile phone manufacturer.

-

IT Hardware & Component Ecosystems: Incentivizing localized fabrication of printed circuit boards (PCBs), display units, camera modules, sensors, and precision mechanical components to systematically scale up domestic value addition.

-

Strategic Material Security: To prevent vulnerabilities in the deep tech supply chain, the government has extended vital structural support across allied sectors. This includes deep-tier frameworks like the ₹7,280-crore Rare Earth Permanent Magnet (REPM) Manufacturing Scheme, which secures specialized components required for clean energy, advanced robotics, EV motors, and automated wafer-handling machinery.

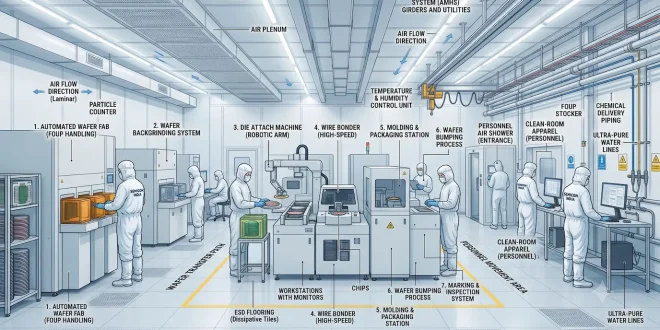

The Semiconductor Roadmap Takes Shape

India is successfully advancing past the design phase into physical silicon assembly, testing, packaging, and commercial fabrication. Under the modified India Semiconductor Mission (ISM), multiple mega-facilities are moving rapidly through execution phases:

-

Commercial Outsourced Semiconductor Assembly and Test (OSAT) Plants: Key facilities launched by global giants like Micron Technology alongside local industrial powerhouses (such as Kaynes Semicon, CG Semi in partnership with Japan’s Renesas, and Tata Electronics in Assam) are actively converting raw wafers into finished memory chips and specialized automotive ICs.

-

The Mega-Fab Frontier: Construction continues to scale at the monumental Tata Semiconductor Plant in Dholera, Gujarat, India’s pioneering ₹91,000-crore commercial foundry developed alongside Taiwan’s PSMC. The plant is engineered to process 300mm wafers at mature nodes (28nm and above), laying the groundwork for self-reliance in microcontrollers and power management systems.

Capitalizing on “China Plus One” and Infrastructure Corridors

The macro economic transition is heavily supported by global “China Plus One” supply-chain diversification. To handle the subsequent influx of heavy industrial requirements, India has fortified its physical and technical infrastructure:

-

Multi-Modal Logistics: Massive investments in dedicated freight corridors, modern high-speed expressways, automated digital customs systems, and specialized logistics parks have drastically reduced turnaround times.

-

Decentralized Technology Ecosystems: State governments are creating specialized clusters to absorb advanced components. For instance, the Uttar Pradesh AI Mission is establishing data center hubs in Noida and an AI City in Lucknow, building regional hardware and deep-tech compute backbones.

-

Cross-Sector Synergy: This localized hardware boom directly feeds the rapid expansion of secondary high-tech industries, such as India’s booming defense drone ecosystem, which leverages domestic component pipelines to engineer autonomous systems and achieve military self-reliance.

Addressing Structural Hurdles for Future Dominance

While the milestones achieved are historic, transitioning into a absolute global manufacturing leader requires addressing remaining bottlenecks:

-

Upstream Wafer Reliance: Commercial packaging (OSAT) plants still depend on imported raw silicon wafers before performing domestic assembly and testing.

-

Deep R&D Investment: Moving from mature process nodes (28nm) down to sub-5nm advanced nodes required for next-generation AI silicon and cutting-edge mobile processors will demand massive, prolonged capital expenditure.

-

Advanced Equipment Sourcing: Acquiring complex photolithography machinery remains a global geopolitical bottleneck that requires continuous diplomatic and corporate alignment.

By scaling up domestic value addition, integrating multi-state industrial corridors, and training a specialized technical workforce in automation, robotics, and semiconductor engineering, India is solidly on track to anchor the global electronics ecosystem for decades to come.

Frequently Asked Questions (FAQ)

Q1: What is driving the sudden surge in India’s electronics manufacturing sector?

A: The growth is driven by the government’s financial incentives under the Production-Linked Incentive (PLI) scheme, a large skilled engineering workforce, aggressive infrastructure updates (like freight corridors), and global “China Plus One” corporate supply chain diversification strategies.

Q2: What is the current status of the Tata Semiconductor Plant in Dholera?

A: The ₹91,000-crore Tata Dholera Fab project, developed in collaboration with Taiwan’s PSMC, is actively under construction and scaling its facilities to produce India’s first domestic 300mm silicon wafers at mature nodes (28nm and above).

Q3: How do allied initiatives like the Rare Earth Permanent Magnet (REPM) Scheme help electronics manufacturing?

A: High-grade rare earth magnets are essential for precision hardware components, electronic sensors, defense drones, and automated clean-room equipment used in chip factories. Localizing these materials prevents supply chain disruptions.

Q4: Is India moving toward exporting electronics or just assembling them?

A: India has graduated beyond basic assembly. Electronics are now the country’s third-largest export category, led by smartphones, with localized domestic component value addition expanding to reduce total dependency on foreign imports.

Disclaimer

This article is curated exclusively for educational and informational purposes. The economic metrics, industrial statuses, and policy allocations detailed are compiled from ministerial declarations, global supply-chain updates, and localized industrial performance reports available as of mid-2026.