Mumbai. Wednesday, 15 July 2026

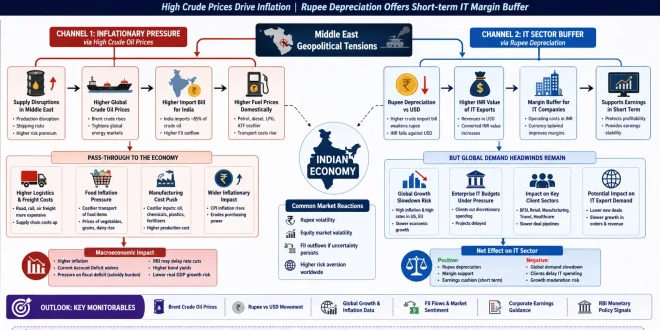

The global financial landscape is shifting rapidly as accelerating geopolitical friction in the Middle East draws intense scrutiny from international markets. For India, a major global economic node, the developments present a complex matrix of challenges and structural cushions. Operating simultaneously as one of the world’s largest importers of crude oil and the undisputed leader in information technology (IT) services, the domestic economy is parsing how energy volatility and fluctuating investor sentiment will dictate fiscal performance through the remainder of the year.

While immediate anxieties concentrate heavily on escalating crude oil price matrices, economic analysts point to a deeper web of cause-and-effect indicators. The evolving regional dynamic is expected to ripple directly into domestic retail inflation, currency valuation models, corporate profit margins, and the long-term pipeline of global digital spending.

┌─────────────────────────────────────────┐

│ Geopolitical Tensions in Middle East │

└────────────────────┬────────────────────┘

│

┌──────────────────────────┴──────────────────────────┐

▼ ▼

┌──────────────────────┐ ┌──────────────────────┐

│ Crude Oil Spikes │ │ Global Risk Aversion│

└──────────┬───────────┘ └──────────┬───────────┘

│ │

├──────────────────────────┐ ▼

▼ ▼ ┌───────────────────────┐

┌──────────────────────┐ ┌──────────────────────┐ │ Western Enterprise │

│ Widening Trade Gap │ │ High Logistical Cost │ │ Discretionary Slowdown│

└──────────┬───────────┘ └──────────┬───────────┘ └──────────┬────────────┘

│ │ │

▼ ▼ ▼

┌──────────────────────┐ ┌──────────────────────┐ ┌───────────────────────┐

│ Rupee Depreciation │ │ Sticky Consumer Price│ │ IT Services Order │

│ (Short-term IT Gain) │ │ Index (CPI) │ │ Pipeline Compression │

└──────────────────────┘ └──────────────────────┘ └───────────────────────┘

The Energy Squeeze: Transmission Channels to Inflation

India relies on foreign oil producers to fulfill nearly 85% of its crude requirements, making its domestic macroeconomic math uniquely sensitive to supply bottlenecks in West Asia. Swift actions by the Indian government—such as tactical updates to energy export policies—highlight the intense focus placed on insulating the local ecosystem from external energy price volatility.

When supply vectors face disruption, the economic impact cascades through four primary domestic channels:

-

Logistics and Distribution Margins: Immediate rises in transportation and freight costs filter into everyday supply chains, increasing the landing price of basic goods.

-

Petrochemical and Input Strains: Industries deeply reliant on petroleum derivatives—such as paints, packaging, specialized chemicals, and plastics—see immediate spikes in base manufacturing expenses.

-

Agricultural Pressures: Secondary impacts hit distribution systems, directly threatening food inflation metrics via elevated freight charges.

-

Monetary Policy Tightening: Persistent strength in global oil benchmarks threatens to undo months of relative stability in India’s retail inflation, potentially prompting the Reserve Bank of India (RBI) to defer highly anticipated interest rate cuts to defend macroeconomic baselines.

The Rupee Cushion vs. The Enterprise Demand Wall

For India’s USD 250+ billion information technology services architecture, the geopolitical crisis introduces a striking contrast between short-term balance sheet inflation and long-term volume threats.

The Accounting Tailwind: Currency Depreciation

As the country’s energy import bill expands, the widening current account deficit naturally exerts downward pressure on the Indian Rupee (INR) against the US Dollar (USD). For premier IT exporters, this currency pivot works as a structural shock absorber. Because these companies bill international clients in hard foreign currencies (predominantly USD and Euros) while supporting their delivery centers using an INR-based cost structure, currency depreciation provides an immediate tactical boost to operational margins.

The Structural Headwind: Tighter Global Wallets

However, this currency advantage cannot completely bypass macro-level demand contractions. A prolonged geopolitical crisis in the Middle East invariably feeds global inflationary pressures, causing enterprise clients across North America and Western Europe to adopt highly defensive corporate postures.

Key IT client verticals—most notably Banking, Financial Services, and Insurance (BFSI), alongside global retail and heavy manufacturing—traditionally respond to geographic instability by freezing discretionary technology spending. While mandatory cloud maintenance and security operations remain sticky, expansive digital transformation initiatives and consulting rollouts frequently face deferred timelines until international economic baselines stabilize.

Structural Winners vs. Sectors Under Pressure

The balance of economic impact varies drastically depending on a sector’s position relative to energy dependency and domestic production mandates:

-

Sectors Facing Strained Profitability: Aviation, logistics, commercial automobile manufacturing, and consumer goods companies experience rapid margin compression if fuel hikes cannot be smoothly transferred to end consumers.

-

Sectors Positioning for Strategic Growth: Upstream oil and gas exploration entities benefit from elevated domestic extraction realizations. Concurrently, national defense manufacturing ecosystems and renewable energy developers see accelerated capital momentum as the country pushes hard for strategic self-reliance.

Fundamental Macroeconomic Buffers

Despite the scale of these external headwinds, India’s modern economic structure stands significantly more insulated than during historic oil shocks. The country’s defense is anchored by robust internal engines: healthy domestic urban consumption patterns, high-performing tax architectures featuring record-breaking GST collections, substantial foreign exchange reserves, and systemic interventions by the RBI to anchor rupee volatility.

The eventual depth of the economic impact rests entirely on the duration of the conflict. While near-term market volatility remains virtually assured, the structural diversification of India’s internal markets acts as a powerful buffer against prolonged macroeconomic distortion.

Frequently Asked Questions (FAQs)

Q1: Why does a higher global crude oil price trigger inflation inside India?

Because India imports 85% of its oil, price hikes instantly raise the cost of importing fuel. This directly drives up transportation, logistics, and manufacturing expenses for products utilizing petroleum inputs, eventually filtering down to consumer retail prices.

Q2: How does a weakening Indian Rupee actually help local IT companies?

Indian IT firms generate the vast majority of their sales pipelines abroad in US Dollars, while paying their domestic workforce and operational overhead in Indian Rupees. When the Rupee depreciates, those US Dollar revenues translate into significantly higher Rupee amounts, short-term bolstering their operating margins.

Q3: What is the primary long-term threat to the Indian tech sector during global geopolitical conflicts?

The ultimate risk is a global economic slowdown. If overseas corporate clients in the US and Europe face inflation and higher interest rates, they often postpone large discretionary investments, freeze tech consulting agreements, and downscale new digital transformation initiatives.

Disclaimer

The information provided in this article is for educational and informational purposes only and does not constitute financial, investment, or policy advice. Market conditions are subject to rapid change based on real-time geopolitical events. Readers should consult with accredited financial advisors before making any investment decisions.

Relevant External Coverage: To trace the historical trajectory of commodities and industrial adjustments related to global market movements, review recent adjustments concerning domestic fuel pricing and tax milestones via the Matribhumi Samachar Economy Dashboard.