New Delhi. Sunday, 26 April 2026

The Atal Pension Yojana (APY) remains a cornerstone of India’s social security net, specifically designed to provide a financial safety net for the unorganized sector. As we move through 2026, the importance of structured retirement planning has never been higher. This guide breaks down the latest contribution charts, eligibility tweaks, and the long-term benefits of joining this government-backed scheme.

What is the Atal Pension Yojana?

Launched by the Government of India and regulated by the Pension Fund Regulatory and Development Authority (PFRDA), APY is a periodic contribution-based pension scheme. It guarantees a fixed monthly income after the age of 60, ranging from ₹1,000 to ₹5,000, depending on your chosen plan and contribution history.

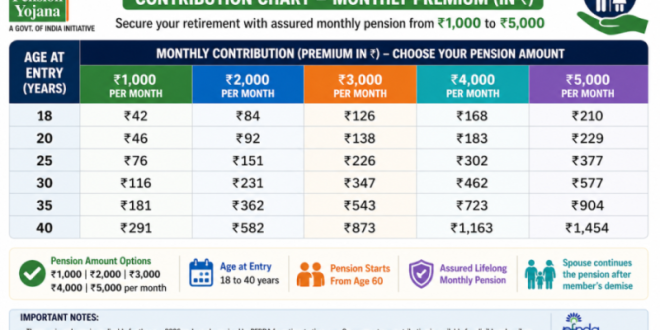

The 2026 Contribution Structure

The core philosophy of APY is “The Earlier, The Better.” Because the corpus has more time to grow, younger entrants pay significantly lower premiums.

APY Monthly Contribution Table (Sample Ages)

| Entry Age | ₹1,000 Pension | ₹3,000 Pension | ₹5,000 Pension |

| 18 Years | ₹42 | ₹126 | ₹210 |

| 25 Years | ₹76 | ₹226 | ₹377 |

| 30 Years | ₹116 | ₹347 | ₹577 |

| 35 Years | ₹181 | ₹543 | ₹904 |

| 40 Years | ₹291 | ₹873 | ₹1,454 |

Critical Eligibility & “The Income Tax Rule”

While APY is inclusive, a major update (effective since late 2022 and strictly enforced in 2026) dictates:

-

Income Tax Payers: Any citizen who is or has been an income tax payer is not eligible to join APY. This ensures the government subsidy and social security focus remain on lower-income groups and the unorganized workforce.

-

Age Bracket: You must be between 18 and 40 years old.

-

KYC Requirements: A savings bank account linked with Aadhaar and an active mobile number are mandatory for the auto-debit facility.

Why APY is a Smart Choice in 2026

-

Inflation Hedge (Triple Benefit): Upon the subscriber’s death, the pension continues for the spouse. After the spouse’s passing, the entire accumulated corpus (up to ₹8.5 Lakhs for the ₹5,000 slab) is returned to the nominee.

-

Tax Benefits: Even though tax-payers cannot join, those who joined before becoming tax-payers can still claim deductions under Section 80CCD (1B).

-

Discipline: The auto-debit feature ensures you never miss a contribution, fostering a disciplined savings habit.

How to Apply

You can enroll via your bank’s mobile app or visit any nationalized bank/post office. Ensure your bank account has sufficient balance on the 1st of every month to avoid small penalty charges for late payments.

Stay Updated with Matribhumi Samachar

For more insights into government schemes and financial literacy, visit these relevant sections:

Note: Many users believe they can increase their pension amount at any time. While you can upgrade or downgrade your pension slab, this is typically allowed only once a year during the month of April. Plan your upgrades accordingly!

Disclaimer

This content does not constitute professional financial or legal advice. Retirement planning involves long-term commitments; therefore, readers are encouraged to consult with a certified financial advisor or visit their authorized bank branch before enrolling in the scheme.