New Delhi. Monday, 4 May 2026

For senior citizens planning their finances in 2026, choosing between the Senior Citizen Savings Scheme (SCSS) and Bank Fixed Deposits (FDs) is a critical decision. While both offer safety, the SCSS currently maintains a clear edge in interest rates, while Bank FDs offer unparalleled liquidity and tenure flexibility.

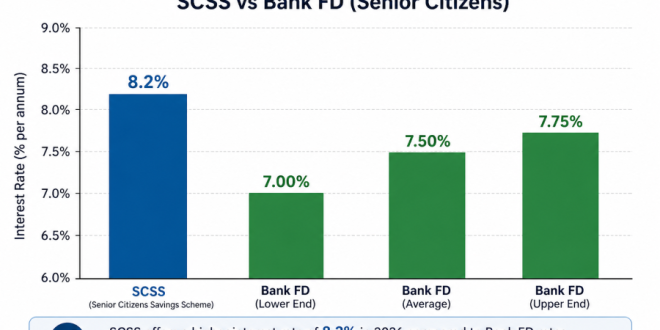

1. Interest Rate Analysis (May 2026)

The interest rate environment in 2026 favors government-backed small savings schemes.

-

SCSS: The Government of India has fixed the rate at 8.2% per annum for the April–June 2026 quarter. Once you invest, this rate is locked for the entire 5-year tenure.

-

Bank FDs: Leading public and private sector banks (like SBI, HDFC, and ICICI) are offering between 6.75% and 7.75% for senior citizens. Some Small Finance Banks (SFBs) like ESAF and Unity offer up to 8.25%, but with different risk profiles.

2. Income Generation: The ₹30 Lakh Test

If a retiree invests the maximum allowed limit of ₹30 lakh into these schemes, the difference in “pension-like” income is significant:

| Feature | SCSS (8.2%) | High-Yield Bank FD (7.5%) |

| Annual Interest | ₹2,46,000 | ₹2,25,000 |

| Quarterly Payout | ₹61,500 | ₹56,250 |

| Monthly Equivalent | ₹20,500 | ₹18,750 |

SCSS provides approximately ₹21,000 more annually than a standard 7.5% bank deposit.

3. Key Features & Operational Differences

Safety and Security

-

SCSS: Sovereign guarantee (backed by the Central Government). It is the safest investment in the country.

-

Bank FDs: Insured up to ₹5 lakh per bank by the DICGC. For a ₹30 lakh investment, SCSS is inherently lower risk than a single bank FD.

Tenure and Extension

-

SCSS: Fixed 5-year term. It can be extended once for an additional 3 years within one year of maturity.

-

Bank FDs: Highly flexible. Tenures range from 7 days to 10 years, allowing you to ladder your investments.

Liquidity and Premature Withdrawal

-

SCSS: Permitted after 1 year but with penalties. 1.5% deduction from principal if closed before 2 years; 1% deduction if closed after 2 years.

-

Bank FDs: Generally more liquid. Most banks allow online premature closure with a 0.5%–1% interest rate penalty, often providing funds within minutes.

4. Tax Implications

Both schemes are subject to the same basic tax laws, but with a specific advantage for SCSS:

-

Section 80C: Investments in SCSS and 5-Year Tax-Saver FDs qualify for a deduction of up to ₹1.5 lakh. Regular FDs do not.

-

Section 80TTB: Senior citizens can claim a deduction of up to ₹50,000 on total interest income from all deposits (SCSS + FDs) in a financial year.

-

TDS: Tax is deducted at source if the annual interest exceeds ₹50,000. Submit Form 15H to avoid TDS if your total income is below the taxable limit.

Final Verdict: Which should you choose?

-

Choose SCSS if: You want the highest possible guaranteed income and have a lump sum you don’t need for at least 5 years.

-

Choose Bank FDs if: You need liquidity for emergencies or want to invest for a shorter period (1–3 years).

Relevant Resources

For more updates on government schemes and financial news in India, visit:

Disclaimer

Interest rates mentioned (8.2% for SCSS and 6.5%–7.75% for Bank FDs) are based on the prevailing market and government notifications at the time of writing. These rates may vary by bank, tenure, and quarterly revisions by the Ministry of Finance. Please verify current rates with your bank or the nearest Post Office.