New Delhi. Sunday, 3 May 2026

In the current financial landscape of 2026, the NPS Vatsalya Scheme has emerged as a cornerstone for parental financial planning. Introduced by the PFRDA, this minor-focused pension model is no longer just a “savings habit”—it is a sophisticated wealth-creation tool that leverages half a century of compounding.

What is the NPS Vatsalya Scheme?

NPS Vatsalya is a contributory pension scheme designed for Indian citizens under the age of 18. It allows parents or legal guardians to open a Permanent Retirement Account Number (PRAN) in the child’s name, which eventually transitions into a standard NPS Tier-I account when the child turns 18.

Latest Updates (May 2026)

-

Revised Entry Barrier: You can now start with an initial contribution as low as ₹250 (down from the earlier ₹1,000 threshold).

-

Global Inclusion: The scheme is now fully open to NRIs and OCI cardholders, provided the bank account used for contributions is NRE/NRO compliant.

-

Aggressive Growth: Guardians can now opt for Active Choice and allocate up to 75% in Equities, maximizing returns during the child’s most significant growth years.

Key Benefits & Features

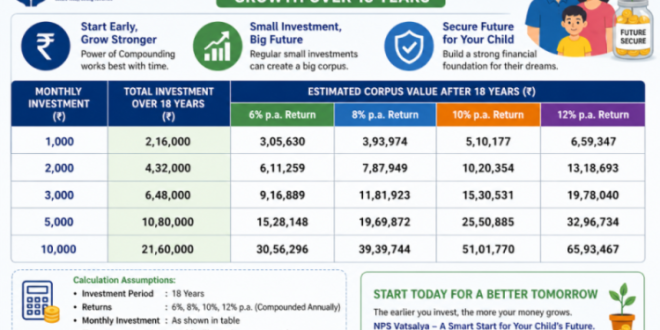

1. The Power of “Hyper-Compounding”

Because the investment starts in childhood, the money has 40–50 years to grow before retirement. Small monthly amounts can lead to a corpus that significantly outperforms traditional savings plans like FDs or child endowment policies.

2. Flexible Asset Allocation

Parents can choose between:

-

Auto Choice: Risk reduces automatically as the child nears age 18.

-

Active Choice: Manually decide the split between Equity (E), Corporate Bonds (C), and Government Securities (G).

3. Withdrawal Rules (New Guidelines)

The PFRDA has streamlined withdrawals to ensure the fund serves its purpose while remaining accessible for emergencies:

-

Education & Medical: Up to 25% of the guardian’s contributions can be withdrawn after 3 years for specific needs (education, specified illnesses, or 75%+ disability).

-

Transition at 18: At majority, the child must complete a fresh KYC. If the corpus is ₹8 lakh or less, they can withdraw 100% as a lump sum. If higher, they can take 20% as cash and must annuitize 80%.

Comparative Advantage: NPS Vatsalya vs. Others

| Feature | NPS Vatsalya | Sukanya Samriddhi (SSY) | Child Mutual Funds |

| Eligibility | All children (Boys & Girls) | Girls only | All |

| Returns | Market-linked (9–13% avg) | Fixed (8.2% approx) | Market-linked |

| Max Limit | No Limit | ₹1.5 Lakh/year | No Limit |

| Control | PFRDA Regulated | Government Backed | AMC Regulated |

How to Open an Account

-

Online (eNPS): Visit the official NPS Trust portal or a CRA website (Protean/KFintech).

-

Offline: Visit any Point of Presence (PoP), including major banks like SBI, HDFC, ICICI, or India Post offices.

-

Documents Needed:

-

Birth Certificate of the Minor.

-

Aadhaar and PAN of the Guardian.

-

KYC documents for NRI/OCI (Passport/Foreign address proof).

-

Pro-Tip: While NPS Vatsalya is excellent for retirement, consider pairing it with a liquid Mutual Fund SIP to cover short-term university costs, as NPS is primarily designed for long-term wealth preservation.

Useful Links from Matribhumi Samachar

For more localized news and detailed financial analysis in English, check these official resources:

Disclaimer

National Pension System (NPS) investments are subject to market risks. Returns are not guaranteed and depend on the performance of the underlying asset classes (Equity, Corporate Bonds, and Government Securities). Past performance is not indicative of future results.