Mumbai. Friday, 1 May 2026

The Reserve Bank of India (RBI) has officially overhauled the “Credit Card and Debit Card – Issuance and Conduct Directions” to favor consumer protection. This move specifically targets the “debt trap” created by rigid penalty structures and immediate reporting of defaults to credit bureaus. By introducing a mandatory buffer and correcting how penalties are calculated, the RBI aims to safeguard users from technical delays or temporary liquidity crunches.

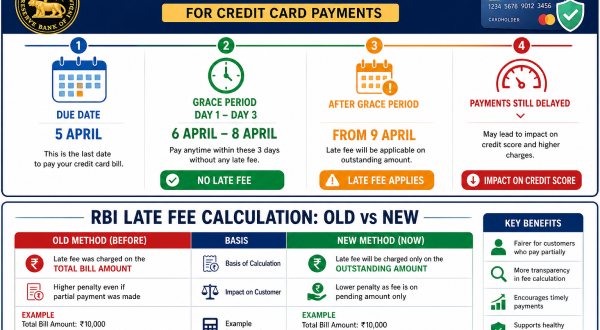

1. The Mandatory 3-Day Grace Period

Prior to this update, many banks would levy a late fee at midnight the moment a due date was missed. Now, the RBI mandates a 72-hour window.

-

Rule: Banks can only report an account as “past due” to Credit Information Companies (CICs) like CIBIL, or levy penal charges, if the payment remains unpaid for more than three days after the due date.

-

The Catch: While you won’t get hit with a “late fee” during these 3 days, the “Days Past Due” (DPD) count for interest purposes still starts from the original due date once you cross the grace period.

2. Fairer Late Fee Calculation

This is perhaps the most significant financial relief. Previously, if you owed ₹50,000 and paid ₹45,000, some banks would still calculate the late fee based on the total ₹50,000.

-

New Rule: Late payment charges and other related penal charges shall be levied only on the outstanding unpaid amount after the due date, not on the total statement balance.

3. Proactive Relief for Natural Disasters

Starting in July 2026, banks are empowered to act as first responders during regional calamities.

-

Immediate Assistance: Banks can offer payment restructuring or extensions without waiting for individual customer applications.

-

Targeted Support: This applies specifically to areas declared affected by state or central authorities, ensuring that victims aren’t burdened with credit score damage while dealing with emergencies.

Quick Reference: Implementation Timeline

| Feature | Old System | New System (RBI Update) | Effective Date |

| Grace Period | Often 0-24 hours | Strict 3-Day (72 hours) | April 1, 2027 |

| Late Fee Basis | Total Bill Amount | Unpaid Balance Only | April 1, 2027 |

| Disaster Relief | Customer must request | Proactive Bank Action | July 1, 2026 |

Important Reminder: While these rules provide a safety net, Interest (APR) still accrues from the date of purchase if the full amount is not paid. The “Grace Period” protects your credit score and penalty fees, but it does not stop the interest clock. Always aim to pay the “Total Amount Due” to remain interest-free.