Mumbai. Friday, 22 May 2026

The battle between aggressive debt collection and borrower dignity has reached a decisive turning point. In a definitive move to dismantle predatory collection ecosystems, the Reserve Bank of India (RBI) has introduced a comprehensive draft framework targeting the strong-arm tactics used by banks and Non-Banking Financial Companies (NBFCs).

Scheduled to take full effect on October 1, 2026, these updated regulations patch long-standing regulatory loopholes, introduce severe financial penalties for non-compliant lenders, and firmly establish a borrower’s right to fair treatment.

⚖️ Redefining Accountability: The Death of the “Third-Party” Excuse

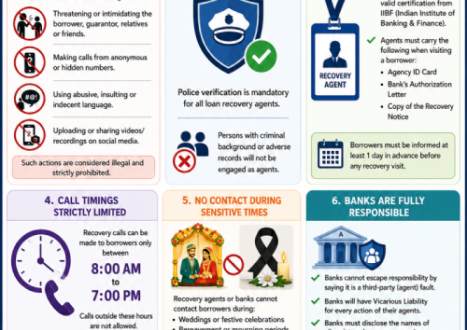

For years, when recovery agents engaged in verbal abuse, public shaming, or physical intimidation, major financial institutions hid behind a corporate firewall. Lenders routinely deflected legal fallout by claiming that rogue collection practices were the independent actions of outsourced third-party agencies.

The RBI’s 2026 framework permanently abolishes this loophole through the absolute enforcement of Vicarious Liability.

1. Direct Institutional Liability

Under the new rules, banks and NBFCs are legally inseparable from the agents they employ. If an empanelled recovery agent violates an RBI code of conduct—such as calling outside permitted hours or using abusive language—the principal lender is treated as the primary violator. This exposes the financial institution directly to regulatory audits, public censure, and hefty institutional fines.

2. The Mandatory “Operational Pause”

One of the most powerful shields given to consumers is the mandatory freeze on collection tracking. The moment a borrower lodges a formal complaint regarding agent harassment or coercive behavior, the bank or NBFC must immediately suspend all recovery actions related to that account. Collection activities can only resume after a formal internal investigation has concluded and a written resolution report is delivered to the borrower.

3. Public Transparency Registries

Lenders can no longer operate anonymous shadow networks of local enforcers. Financial institutions must maintain an up-to-date, publicly accessible database of all registered, empanelled recovery agencies on their official websites and mobile apps. If an agency is terminated due to misconduct, the lender must proactively notify all affected borrowers linked to that agency.

📱 The Digital Frontier: Strict Restrictions on Smartphone Data and Remote Locking

As banking shifted to mobile applications, harassment evolved from doorstep confrontation to digital intrusion. The 2026 guidelines introduce explicit, strict boundaries around digital debt collection, focusing heavily on smartphone privacy and the controversial practice of remote device locking.

Absolute Ban on Device Data Harvesting

Recovery personnel and lending apps are strictly prohibited from accessing, scanning, or storing a borrower’s personal mobile device data. This includes contact lists, personal photo galleries, precise GPS locations, and text messages. Using a borrower’s contacts to shame them into repayment is now classified as a severe, punishable offense.

The “Mobile Lock” Regulatory Matrix

Fintech lenders frequently use embedded software to entirely lock a borrower’s smartphone following a missed Equated Monthly Installment (EMI). The RBI has imposed tight boundaries around this practice to ensure it is not used as a tool for immediate coercion.

[Smartphone Financing Only]

│

▼

[90 Days Past Due (NPA Stage)] ──► [60-Day & 7-Day Staged Warnings] ──► [Execution of Lock]

│

▼

[Emergency Call Access Maintained]

Lenders must adhere to the following operational parameters:

-

Financing Alignment: A smartphone can only be remotely locked if the loan itself was explicitly extended to purchase that specific device. Locking a user’s personal phone for a general personal loan or an unrelated line of credit is strictly illegal.

-

Staged Timeline Warnings: Devices cannot be locked immediately upon a missed payment. The loan must officially cross into Non-Performing Asset (NPA) status (90 days past due). Furthermore, the lender must issue explicit warnings at the 60-day and 7-day marks before deploying a digital lock.

-

Preservation of Essential Life Services: Even when a device is legally locked, it cannot be rendered completely useless. The smartphone must maintain basic connectivity, including incoming cellular calls, access to high-speed internet for banking/educational functions, emergency SOS dialing, and public safety alerts.

⚠️ The Hourly Penalty Clause: If a borrower clears their overdue balance or reaches an official settlement, the lender must unlock the smartphone within one hour of payment validation. Failure to do so triggers a mandatory statutory compensation rate of ₹250 per hour, payable directly to the borrower for every hour the device remains wrongfully locked.

⏱️ Strict Professional Boundaries and Timing Windows

To restore civil boundaries to the loan recovery process, the RBI has defined rigid operational windows and mandatory training prerequisites for all collection staff.

-

The 8:00 AM to 7:00 PM Boundary: Recovery agents are legally barred from contacting borrowers via phone calls or physical visits outside the hours of 8:00 AM and 7:00 PM.

-

Sanctity of Sensitive Occasions: Agents are forbidden from visiting or calling a borrower during deeply sensitive personal periods, including funerals, active mourning phases, or major milestone family functions like weddings.

-

Advance Visit Notification: Surprise physical visits are a thing of the past. Borrowers must receive a digital alert (via SMS or verified email) at least 24 hours prior to an agent arriving at their doorstep. If digital contact fails, a formal physical letter must be delivered 3 days in advance.

-

The Professional Credential Protocol: Every visiting recovery agent must actively carry and present three items before commencing any discussion: a valid Indian Institute of Banking and Finance (IIBF) certification, an official agency ID card, and a direct authorization letter issued by the lending bank or NBFC.

🛠️ Step-by-Step Grievance Protocol for Borrowers

If you find yourself facing coercive, abusive, or non-compliant actions from loan recovery agents, do not suffer in silence. Use this precise, step-by-step framework to activate your consumer rights under current Indian financial regulations:

🔗 Relevant External Context & Reference Links

To stay informed on broader policy perspectives, localized regional implementations, and systemic consumer rights notices, review the following external resources:

-

For real-time coverage of Indian economic mandates, legal declarations, and regional administrative updates regarding banking consumer protection laws, check out the English news portal at Matribhumi Samachar.

-

To read official regulatory press releases, view the complete master circulars on debt collection, or verify the registration status of non-banking lenders, visit the Reserve Bank of India Official Portal.