New Delhi. Updated on : Sunday, 9 August 2026

Women’s empowerment in India has undergone a major paradigm shift, transitioning from traditional social welfare programs into a vital driver of economic policy. As of 2026, government frameworks are designed to foster long-term financial independence, maternal health, rural entrepreneurship, and tech-driven livelihoods.

This detailed guide breaks down the core government schemes empowering women across the nation, complete with the latest policy updates, revised financial thresholds, and key takeaways.

1. Maternal Health & Direct Welfare

Pradhan Mantri Matru Vandana Yojana (PMMVY) 2.0

The PMMVY framework directly addresses maternal nutrition while encouraging gender parity right from birth.

-

Primary Benefit: Eligible pregnant and lactating mothers receive a direct financial benefit of ₹5,000 for their first child, delivered in installments to compensate for wage loss and support nutrition.

-

Key Policy Enhancement: To discourage female feticide and balance the child sex ratio, the government offers an enhanced benefit of ₹6,000 for the second child, provided the second child is a girl.

-

Digital Process: Fund disbursal is streamlined through direct bank transfers using the PMMVY Soft App.

Pradhan Mantri Ujjwala Yojana (PMUY)

PMUY leads India’s clean energy transition by providing vulnerable households with accessible, subsidized Liquefied Petroleum Gas (LPG).

-

Simplified Access: Urban poor and migrant families can register using a self-declaration address proof alongside basic identity credentials, bypassing traditional paperwork bottlenecks.

-

Targeted Subsidies: Program beneficiaries receive a targeted subsidy of approximately ₹300 per cylinder, helping sustain clean cooking practices.

2. High-Yield Savings & Financial Security

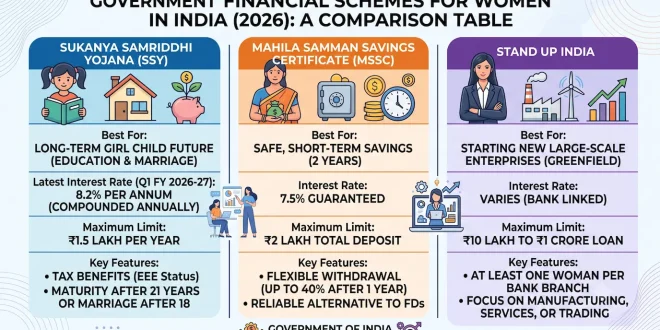

Sukanya Samriddhi Yojana (SSY)

Designed to build long-term financial security for the girl child, SSY remains one of the highest-yielding government-backed small savings vehicles.

-

Interest Rate: Offers 8.2% per annum (compounded annually).

-

Tax Exemption: Enjoys full EEE (Exempt-Exempt-Exempt) status under Section 80C, rendering investment principal, interest accrued, and final maturity tax-free.

-

Tenure: Accounts mature 21 years from account opening or upon the girl’s marriage after attaining 18 years of age.

Mahila Samman Savings Certificate (MSSC)

MSSC serves as a safe, guaranteed short-term investment option tailored specifically for female investors.

-

Fixed Returns: Delivers a guaranteed 7.5% per annum fixed interest over a 2-year tenure.

-

Deposit Limits & Partial Withdrawal: Accommodates deposits up to an aggregate cap of ₹2 lakh, with a partial withdrawal feature of up to 40% permitted after one year.

3. Credit Access, Rural Livelihoods & Tech Initiatives

Lakhpati Didi & Drone Didi Initiatives

Synchronized under the Union Budget initiatives, this dual model drives economic independence within rural Self-Help Groups (SHGs).

-

Lakhpati Didi: Expands skill training and supply chain linkages to enable 3 crore SHG women to achieve a sustainable annual net income of at least ₹1 lakh.

-

Drone Didi: Provides technical certification and hands-on training to 15,000 SHG members to pilot drones for precision agriculture, crop monitoring, and liquid fertilizer application.

Stand Up India & Mudra Yojana

Institutional credit pathways designed to bridge capital gaps for aspiring and established women entrepreneurs.

-

Stand Up India: Requires bank branches to extend collateral-free loans between ₹10 lakh and ₹1 crore to at least one woman entrepreneur per branch for establishing new (Greenfield) ventures in manufacturing, services, or trading.

-

Mudra Yojana: Scaled lending limits under the “Tarun” category ensure priority processing and higher capital accessibility for women-led micro-enterprises.

She-Mart & E-Commerce Integration

-

Digital Market Access: She-Mart connects indigenous creators, rural SHGs, and local artisans directly to global consumer markets through dedicated digital storefronts.

-

Digital Literacy: Handled under the Mahila Shakti Kendra network, offering practical modules on online shop management, digital payment processing, and e-commerce logistics.

Key Financial Schemes Comparison Matrix

| Scheme Name | Interest Rate / Yield | Investment / Loan Cap | Primary Objective |

| Sukanya Samriddhi Yojana (SSY) | 8.2% p.a. (Compounded) | ₹1.5 Lakh / FY | Long-term higher education and marriage fund for girl child |

| Mahila Samman Savings Certificate | 7.5% p.a. (Fixed) | ₹2 Lakh total pool | Secure 2-year short-term savings |

| Stand Up India | Bank Base-linked | ₹10 Lakh to ₹1 Crore | Capital financing for new women-owned enterprises |

Frequently Asked Questions (FAQs)

Q1. Who qualifies for the enhanced ₹6,000 benefit under PMMVY 2.0?

The ₹6,000 benefit applies specifically to eligible pregnant and lactating mothers upon the birth of their second child, provided the child is female. The first child benefit stands at ₹5,000 regardless of gender.

Q2. Is a woman allowed to open multiple MSSC accounts?

Yes. An eligible individual or guardian of a minor girl can open multiple Mahila Samman Savings Certificate accounts, provided the total cumulative deposit across all accounts does not exceed ₹2 lakh and a minimum interval of 3 months is maintained between account openings.

Q3. What documentation is required for migrant workers under PMUY?

Migrant women do not require proof of permanent residence. Registration requires an Aadhaar card, bank account details for subsidy routing, and a simplified self-declaration confirming their current residential address.

Related Coverage & News Updates

For more updates on national policy, social welfare programs, and economic reforms, visit Matribhumi Samachar English or browse through dedicated policy analysis in the Matribhumi Samachar National Section.

Disclaimer

This article is published for informational and educational purposes only. Interest rates, administrative guidelines, and eligibility requirements for government schemes are subject to official policy notifications issued by the respective Ministries and Government of India departments. Readers are advised to verify details with official portals or local branch officials before making financial investments.